The Taxing Challenge- How to Navigate the Difficulties of Calculating Adjusted Cost Basis

March 14, 2024 10:00 AM MST

Correctly calculating the adjusted cost basis for tax reporting can be a very daunting task for many investors.

It is a critical factor in determining the capital gains taxes owed or the losses or deductions that can be taken for the sale of stock, mutual fund or other investment. However, the path to understanding and accurately calculating your adjusted cost basis starts with the answer to this question - What is cost basis? Cost basis is simply the original purchase price of a security. Calculating an adjusted cost basis starts with the purchase price and then adjusts the price for any and every corporate event (splits, mergers, dividends reinvested, etc.) that happened during your holding period. Netbasis, an online cost basis calculator, can help you to navigate all of the complexities that you may encounter when reporting your investment gain or loss.

1. Covered vs. Non-Covered Shares

You’ve probably noticed on your 1099-B that the cost basis for “Covered” shares is provided but not for “Uncovered.” “Uncovered” shares were purchased on or before December 31, 2010. “Covered” shares were purchased on or after January 1, 2011. Although it is next to impossible to get the cost basis or price for those “Uncovered” shares on your own, the IRS requires you to provide the adjusted cost basis for the entire holding period covering the sale or sales.

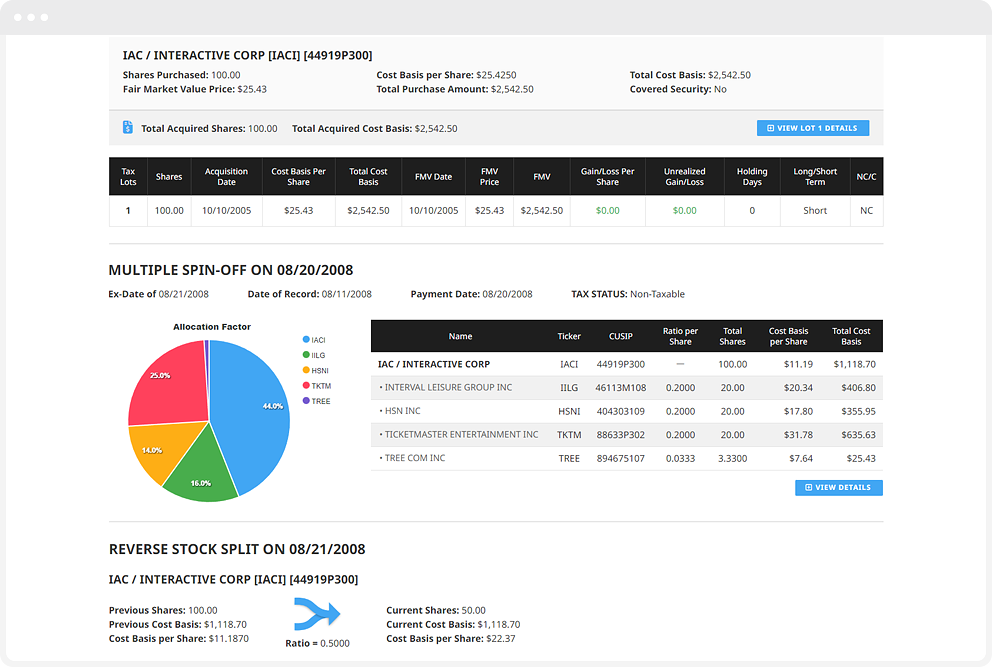

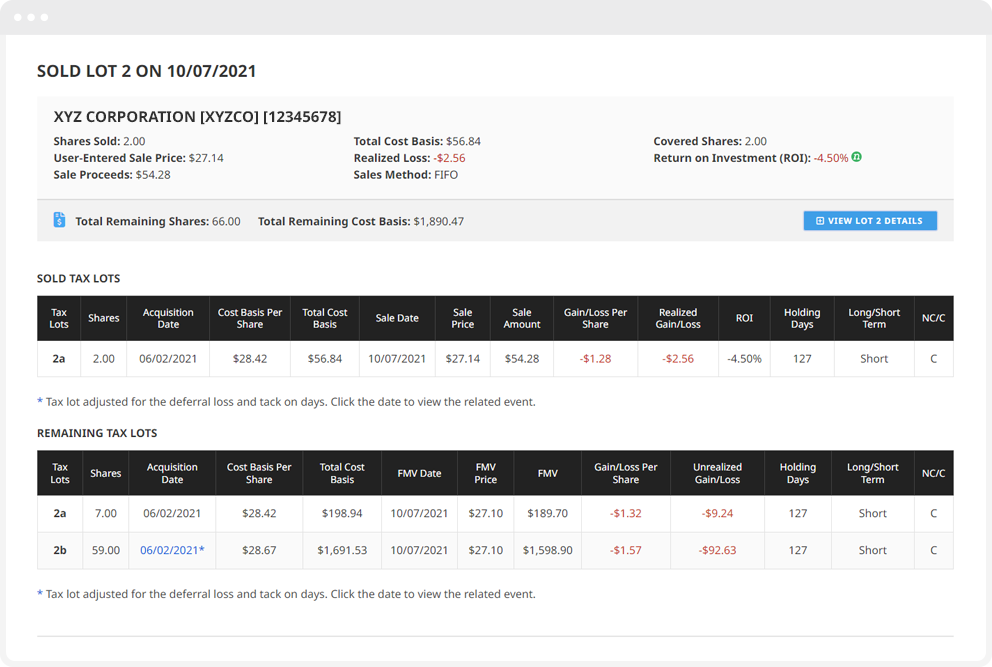

2. Corporate Actions and Events.

Corporate actions such as stock splits, mergers, spin-offs, or dividend reinvestments are complicated adjustments that can have a significant impact on your adjusted cost basis and shares. The cost basis must be adjusted for each event, and failure to correctly account for these changes can lead to inaccurate tax reporting.

3. Wash Sales

Wash sale rules can be very challenging for an investor. First understanding the rules may help investors steer away from this type of investment transaction. A wash sale is identified when selling a security at a loss and repurchasing a substantially identical security within 30 days. Investors must carefully identify and adjust for these transactions to avoid unintended consequences in their tax obligations.

4. Inherited Investments

For investments that were inherited, a tax rule called “Step-Up Cost Basis” is used as the original basis for the security. The investor must determine the price or basis of the inherited shares at the time of the original owner's death instead of the actual original purchase date.

5. Cryptocurrency Complexity

The rise of cryptocurrencies and digital assets has presented a new investment and regulatory landscape. As the tax rules are currently being defined, the end result will most likely require accurate tax reporting of gains or losses.

6. Frequent Trading and Tax Implications

Active traders face challenges of managing the tax implications of frequent buying and selling. The high volume of transactions requires a strategic approach to minimize tax liabilities and optimize overall tax outcomes.

7. Record-Keeping Struggles

Although maintaining meticulous records throughout the year is critical, but often, current record keeping isn’t the issue. Trying to find old records of securities purchased before 2011 (Non-Covered shares) can be a huge challenge for investors. A lot of people struggle with finding original purchase dates, original number of shares purchased or having a record of each transaction if they participated in a Purchase Plan. These issues could potentially result in inaccurate tax reporting.

8. Conclusion

In the very complex world of investing, it is imperative for investors to keep one eye on the tax implications of their investments. Netbasis (www.netbasis.com) is an online cost basis calculator that automatically calculates an adjusted cost basis for securities going back as far as 1925. Netbasis has pricing, corporate actions and dividend information and only requires buy and sell dates of the investor.

POPULAR TOPICS

CRYPTOCURRENCIES

TAX MANAGEMENT